View Current Newsletter -

Search The Archive

Sign Up - Print

Issue

119

Article

204

Published:

6/1/2005

Sarah Friede, Legal Counsel and Vice President, STEC

As more taxpayers, realtors, and accountants become aware of reverse exchanges, the more it becomes an appealing option for a wide array of taxpayers. Some opt for reverse exchanges because they dont want the perfect piece of replacement property to slip through their fingers while they wait for their anticipated relinquished property to sell. Others see the potential for major construction improvements that can be made to a vacant or under-developed lot with proceeds from the sale of relinquished property. Whatever the reason, there are lots of taxpayers who want to do a reverse exchange but dont understand how it is structured, and too often, taxpayers do not seek assistance from their attorneys or a Qualified Intermediary until it is too late. We hate to see that happen and strive to provide as much information and assistance as possible to our attorneys, in the hopes they can helping their clients take advantage of this great tax shelter

One of the most common reasons for losing the opportunity to do a reverse exchange is that taxpayers do not tell their attorneys about their intentions until after the replacement property has been deeded into the taxpayers. Once the deed has been delivered to the taxpayer rather than an Exchange Accommodation Titleholder (or EAT), there is no opportunity for executing a reverse exchange. The taxpayer is prohibited from having simultaneous control of both the replacement and relinquished properties. Rather, one of the properties must be parked with an EAT (normally, a single-member, single-purpose limited liability company created by a Qualified Intermediary for that very purpose) while the other property remains under the taxpayers control. Statewide Exchange Corporation (STEC) strives to have LLCs already on hand in the event of a reverse exchange "emergency", and, under most circumstances, can provide an LLC and exchange documents with just a few hours notice. By having LLCs already formed with the Secretary of States office, we hope to be able to provide better service to attorneys who call us as their clients are sitting down at the closing table.

Another common reason that taxpayers lose the opportunity to do a reverse exchange is that they have selected a lender that does not have flexible underwriting guidelines and refuses to permit an LLC to be in the chain of title (as it will have to be when replacement property is parked). If taxpayers fail to contact an intermediary or inform their attorneys well in advance of closing, there may be no opportunity to inquire of other lenders. STEC has done business with a number of small banks in North Carolina that have knowledgeable personnel and flexible underwriting guidelines, so loan officers can see the transaction as a whole. These banks have no problems lending money to qualified taxpayer-borrowers even though an LLC is taking title and will be signing the deed of trust.

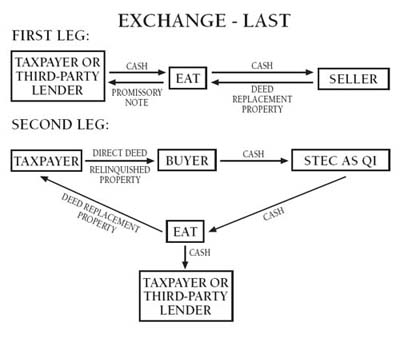

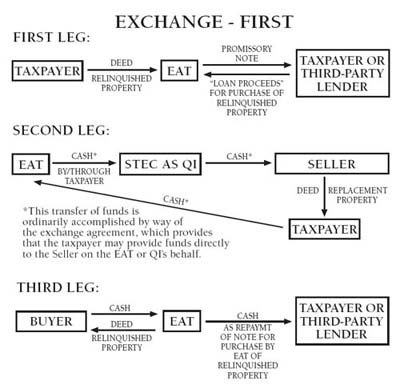

We understand, however, that not all taxpayers are in a position to switch lenders. Our ordinary procedure has been to park replacement property in the name of an LLC of which STEC is the sole member/manager. In order to accommodate financial underwriting guidelines, however, we can also offer a form of reverse exchange in which relinquished (rather than replacement) property is parked in an LLC. What we tend to call a regular reverse exchange is more properly called an "exchange-last" reverse exchange, and this type of parking transaction is considered an "exchange-first" reverse exchange.

Here is a diagram of what an exchange-last looks like (i.e., parking the replacement property):

In contrast, here is what an exchange-first reverse exchange looks like:

As discussed above, doing an exchange-first reverse exchange completely avoids entanglements with loans secured by replacement property because the LLC does not take title to the replacement property. Putting the LLC into the relinquished property chain of title alleviates lenders concerns and permits more taxpayers to take advantage of reverse exchanges.

There are three potential drawbacks to the exchange-first structure that attorneys and taxpayers must be aware of, however. The first potential drawback is that because the relinquished property must be parked before the taxpayer takes title to the replacement property, there is no identification period; thus, there is no opportunity to sell a different piece of investment property if the sale of the parked property is not accomplished by the end of the exchange period. The exchange-last structure permits taxpayers the traditional 45-day identification period in which to identify multiple properties to sell in order to complete the exchange. If their preferred relinquished property does not sell in a timely manner they can make efforts to sell alternate relinquished properties. The exchange-first structure does not permit this sort of back-up plan. For taxpayers who do not own multiple investment properties, however, or are confident the parked relinquished property will sell, this problem is avoided.

The second potential drawback to the exchange-first transaction is that the local Register of Deeds may insist on collecting excise stamps twice, once when the property is transferred to the LLC and once when the LLC transfers the property to the buyer. The deeds must recite that consideration was paid in order to comply with IRS regulations, which most 1031 experts view as being satisfied in the form of the exchange fee paid to the EAT. It is possible that Registers may view the deeds as they would other deeds for consideration (as opposed to gift deeds). Because the transfer of assets from the LLC to the taxpayer could just as easily take the form of transferring ownership in the LLC itself (and indeed in many exchanges, that is how the transfer is accomplished), and because the transfer of the LLC to the taxpayer does not trigger any sales tax, a deed from the LLC should likewise not trigger any taxes. We have spoken with several Registers who seem to understand the nature of exchanges and have assured us that they would not charge excise or transfer stamps. Nonetheless, we advise attorneys to ask their local Registers what their policies are so as to avoid any unpleasant surprises.

The third and final potential drawback to an exchange-first transaction is that a lender with a secured lien on the relinquished property may consider the transfer to trigger a due-on-sale clause. How likely lenders are to find out that the property has been parked is unknown, and STEC would never recommend to taxpayers that they knowingly violate the terms and conditions of existing deeds of trust. This problem should be easily resolved, however, by explaining to the lender that the LLC holds the property in a sort of trust for the taxpayers benefit, and that the property is going to be sold within a matter of months as part of the exchange anyway.

Attorneys and their clients should also be aware that the exchange-first structure does not permit build-to-suit scenarios, in which vacant or under-developed land is purchased and improved with exchange proceeds. Such replacement properties can be parked with an EAT and improved, so that when they are deeded to the taxpayer, the taxpayer takes title to the property with a fair market value that includes the value of construction and up-fitting. Once a taxpayer has actual ownership of the property, the value of the property in the exchange is set and cannot be increased. Any improvements made after the taxpayer takes title are considered not like-kind to real property and will be excluded from the exchange. So, parking the relinquished property with the EAT while constructing improvements on replacement property already vested in the taxpayer is not a situation that is permitted by Section 1031.

Find out more about exchanges at 1031STEC.com

- Home

- ALTA Best Practices

- TRID

- Register of Deeds

- Calculator

- Forms

- Priors

- Commercial

- Newsletters

- What Is Title Insurance?

- News

- Your ?'s

- About Us

- Contact Us

- History

- Rates

- Ratings

- Our Creed

- En Español

- Privacy

Resources

Statewide Title, Inc. is a member of ALTA®, the NCLTA and the FEA.